The UK, European Union and Swiss markets will together switch to a T+1 settlement cycle on 11 October 2027. Many others have already taken the step, including the United States, Canada, Mexico, Argentina, China and India. Improving settlement efficiency and reducing counterparty risk by shifting to T+1 is therefore crucial to enhancing European market competitiveness, as Arnaud de Tregomain, COO & Head of Business Development, Global Markets, BNP Paribas, noted during the bank’s recent event,Towards T+1 in Europe – from Regulation to Reality.

Navigating the transition to T+1 in Europe will be complex. Europe’s market landscape is far more fragmented than the US, with multiple trading venues, currencies, central counterparties (CCPs), central securities depositories (CSDs), regulators, and legal and fiscal frameworks to coordinate. Orderly implementation will demand close collaboration between market participants across business lines and functions – underscoring the value of events like these that bring policy leaders and market practitioners together to share updates and best practice guidance.

Table of Contents

- Navigating the transition to T+1 in Europe: where are we and what should we be doing now?

- Navigating the transition to T+1 in Europe: What are the impacts on market players’ business activities?

- What does shortening the settlement cycle to T+1 mean operationally?

- Navigating the transition to T+1 in Europe: What is the plan for industry testing?

Key takeaways – Navigating the transition to T+1 in Europe

• In a T+1 environment, firms will have 20% of the time that is available today to do 100% of the work.

• Industry participants must meet a series of interim deadlines on the way to 2027 go-live.

• From October 2027, stock loan liquidity sourcing, borrowing, collateral arrangement and settlement must happen by early afternoon on T+0 to give DvP sell trades time to settle.

• A proposed net/batch settlement ‘gating event’ at 11:00 CET across all EU CSDs aims to maintain current settlement netting and funding optimisation for part of EU repo trades that may move to same date settlement to enable funding of their underlying cash bonds trades.

• Better and earlier FX arrangements, such as pre-funding, will be key to avoid funding issues, particularly for APAC investors investing into European-domiciled funds.

• With capital markets around the world moving to T+1, EU-exposed funds are asked to move to T+2 fund settlement.

• Full automation of end-to-end processes, standardisation & collaboration are table stakes for industry participation.

• The EU, UK and Swiss T+1 taskforces recently published a five-pillar testing plan to help industry participants assess their operating models’ readiness for T+1.

• 2026 is the year of action; T+1 success can’t happen by chance or by accident. Each of the industry participants making up the full chain must understand what’s at stake, align processes, work closely with tech providers, financial service providers, outsource suppliers, and FMIs.

• The acceleration of the T+1 execution plan and the preparedness for 2027 year of industry E2E testing are key for a successful go-live with as little as possible after care costs and effort post October 11th, 2027. BNP Paribas, as a European leading actor in the financial industry, is well connected with the UK, EU, and Swiss T+1 governance as well as European regulators, and is ready to act as clients’ preferred solution provider.

Navigating the transition to T+1 in Europe: where are we and what should we be doing now?

T+1 settlement entails a tectonic shift in post-trade processes, procedures and practices. And success will depend on the whole market moving in unison to maintain market integrity, stated UK Accelerated Settlement Taskforce Chair Andrew Douglas during the event’s introductory session.

Douglas’ key message is to have a plan and execute it through continued, focused action. The transition go-live may be October 2027, but regulators expect industry participants to meet a series of interim deadlines along the way. Key among them is that by 31 December 2026, trade allocations and confirmations between buy-side firms and executing brokers should be completed as soon as possible but no later than 23:00 on trade date in Europe and 23:59 in the UK.

The UK Financial Conduct Authority (FCA) will take a more intrusive approach to engagement with supervised entities, and require evidence of firms’ plans, Douglas warned. The T+1 settlement cycle is more than just a compliance imperative though, Douglas added. It is a business necessity – and opportunity to automate, build relationships with firms keen to rationalise their counterparty risks, and future-proof your operations for the digital agenda.

In a T+1 settlement environment, firms will have 20% of the time available today to do 100% of the work. “That is a big ask if you do not automate,” he said.

Douglas cited a US survey that found the 30% of asset managers that failed to prepare in the three months before the T+1 settlement cycle go-live experienced post-implementation cost increases of 16% to 18%, driven mainly by extra headcounts. “In an industry where you measure gains in basis points, to watch 18% of your cash fly out the back door because you didn’t pay attention is not a good result.”

| Client Event Towards T+1 in Europe – from Regulation to Reality To help its clients navigating the transition to T+1 in Europe, BNP Paribas hosted an event in its London offices, and roadshows across Paris, Madrid and Milan, designed to simplify this complex topic and provide clarity on how to prepare. A final, virtual session is planned for September. As well as the bank’s own experts from its Global Markets and Securities Services business lines, the events featured leading speakers from organisations including: • The chair of UK T+1 Accelerated Settlement Taskforce • The independent chair of EU T+1 Industry Committee • Euronext • The Investment Association • Pirum • AMAFI • ISLA • DTCC • Value Exchange • Members of the EU T+1 taskforce Industry Committee The programme examined the business and operational impacts, detailed timelines, and a full presentation of the Industry Testing plan. Audience members interacted with speakers throughout the day to clarify concerns and raise issues in real time, helping navigate this potentially daunting topic, and provide clear actionable guidance for aligning processes, upgrading technology, and coordinating with counterparties. BNP Paribas is available to test with clients at any point. Please contact us if you have any questions or seek more information and/or assistance on the key steps to T+1 and solutions to help you get there. |

Navigating the transition to T+1 in Europe: What are the impacts on market players’ business activities?

Session two moderator Leda Mehilli, Head of GM Infrastructure Solutions & GM Business Sponsor of EU/UK/Swiss T+1 Programme, BNP Paribas, observed that T+1 is a fundamental change in how the business needs to operate, not just settle. Compressing the transaction lifecycle drags almost all the risk, funding and collateral decisions onto trade date, and time differences between Europe, America and APAC clients exacerbate funding and FX exposures.

The session explored these fundamental changes and how they will impact different business lines. Several themes emerged.

T+1 settlement cycle impact on stock lending:

Stock lending activities, part of Securities Financing Transactions (SFT), are among the most heavily impacted by the T+1 transition, despite their explicit exemption from the EU T+1 regulation. In a T+2 cycle, stock loan short coverage takes place on T+1 to allow a full day to secure liquidity, borrows and prepare for settlements, noted Dan Sofianos, Head of Prime Services Supply Trading EMEA, Global Markets, BNP Paribas. From October 2027, sourcing liquidity, borrowing, arranging for collateral and settlement must happen by early afternoon on T+0 to give time to settle the DvP sell trades. That throws up a range of trading and operational issues, including:

- Meeting short needs – Borrowers may need to invest more in net buy-sell trade date activity processing capabilities to calculate short needs faster, along with automated early borrowing and follow-the-sun activity to help with borrowing securities in APAC or US hours. “But that does need flexibility from lending firms as well to adapt to cross-regional trading, collateralisation and instruction release,” said Sofianos.

- Late recalls – Borrower desks have less time to react to late recalls on trade date and return them in time for settlement, so it’s important that buy side sale notifications are sent to the lenders and processed as quickly as possible after execution. If delays occur, lenders may feel under pressure to increase buffers, “which means less liquidity for the short side of the market and less revenue for beneficial owners and long-only lenders,” Sofianos noted.

- Collateral velocity – Turnaround times at triparty agents where most collateralisation happens are a concern, with delays sometimes between when collateral is posted to the lender’s triparty account and loan release. Vendor solutions can help reduce that friction, said Sofianos.

Tony Holland, Director Market Practice with ISLA, highlighted multiple areas where progress with SFTs is being made though.

- UK SLO/SLRs – A control has been agreed between ISLA members and CREST that allows Stock Loan Outbounds and Stock Loan Returns to take place on the same day so borrowers, where necessary, can return loans, rather than having to wait for an SLR to be set up the next day. He also shared the main benefits of being able to move collateral on a same-day basis.

- Corporate action events – The objective is to ensure correct entitlements are passed through the settlement chain. ISLA is working with members to create a potential harmonisation solution across various EU markets, Holland noted.

- DvP deadline – Following the EU T+1 SFT technical workstream meetings, a recommendation has been made to potentially move the T2S DvP deadline from 16:00 to 17:00 CET, whereby one main SBL benefit would be to allow the use of free payment stocks for an additional hour to settle DvP trades, helping increase settlement efficiency and reduce CSDR cash penalties.

T+1 settlement cycle impact on repo:

EU markets, unlike the UK, have a limited O/N repo market in the current T+2 environment. Part of repo trades are anticipated to move to same day T+0 settlement to fund their underlying T+1 cash bonds. The EU SFT Optimisation Taskforce, newly-created by the EU Industry Committee, will suggest further measures ahead of the T+1 settlement cycle implementation date to optimise SFT settlement.

This Taskforce has proposed a new ‘gating event’, a net/batch settlement cycle at 11:00 CET across all EU CSDs to help maintain current levels of netting and settlement optimisation. Salah Amraoui, Deputy Head of Fixed Income Repo, Global Markets, BNP Paribas, welcomed the initiative for fixed income repo. Specifically, for long-short strategies, settlement could be calibrated to enable position squaring and reduce intraday liquidity lines, he said. “So it gives you that window to fund your book.”

However, without strong safeguards parties may pull positions out of the overnight batch and into the gating event, delaying settlement and hence onward deliveries, causing bottlenecks across the market. BNP Paribas is working with peer repo dealers, ISLA, ICMA, AFME and other industry working groups to find ways to best mitigate this risk.

T+1 settlement cycle impact on FX and Funding:

FX timing, funding certainty and cut-offs pose a challenge, particularly for APAC investors investing into European-domiciled funds.

As Investment Association Investment Operations Policy Lead Jermaine Nooks pointed out, T+1 pulls the FX process forward, often into thin APAC/EU overlap windows, squeezing the time available to fix any issues and increasing risk. Better and earlier FX arrangement is key. “You need to have that base currency available to invest and go through your FX processes to think about what is going to be the best solution for your situation,” such as pre-funding to gain earlier funding certainty, or running tight intraday liquidity procedures, said Nooks.

T+1 settlement cycle impact on fund settlement cycles:

With capital markets around the world moving to T+1, it makes sense for the fund industry to move with it, said Nooks. “For EU-exposed funds, the recommendation is clear: move to T+2 fund settlement.”

Work is underway to explore what makes sense for firms so, as an industry, we can present these explainable scenarios to the regulators, Nooks added.

What does shortening the settlement cycle to T+1 mean operationally?

The third panel session kicked off by dissecting the impact of T+1 on asset managers’ operating models, hosted by James Maher, Global Head of Change & Design for Prime and Securities, and Operations Lead for EMEA T+1, BNP Paribas.

Disappearing time buffers will switch the focus for all operational activities to trade date, said David Armstrong, Head of Global Middle Office Market Connectivity and Third-Party Relationships, BNP Paribas Securities Services. For BNP Paribas, that means reviewing end-to-end workflows, including where third parties are involved in processes, to identify challenges that cause non-STP flows and failed trades; target exceptions; and work with those third parties, their platforms and our clients to solve any issues.

Among the challenges highlighted by Armstrong that industry participants need to address are:

- Whether existing FX models are workable for T+1 in Europe – potentially delegating more FX management to custodians or outsourcing to third parties.

- The ability to book trades on trade date, especially for APAC clients that don’t have a Europe time zone presence – where vendor tools that automate booking of the fills could be a solution.

- Knowing the Place of Safekeeping (PSAF) of your assets and ensuring the earliest agreement on Place of Settlement (PSET).

- Use of partial settlement – given 60% to 70% of buy-side trade fails are due to shortage of stock, increased partial settlement use will be crucial to help manage the number of fails.

Accelerating allocations and confirmations is an operational imperative, noted Igor Gramatikovski, Product Management Director, Institutional Trade Processing, DTCC Europe. “We really need to be moving toward a near-real time allocation and confirmation process,” he said. “Solutions for that exist today.”

Full automation becomes table stakes for industry participation, argued Gramatikovski. Removing any end-of-day batch allocations and manual touchpoints is essential.

Standard Settlement Instructions (SSIs) – which specify the “where” of delivery/settlement – will be a key part of the solution. Last year, Euroclear reported 21% to 30% of all securities fails are due to SSIs, said Emma Johnson, Head of Industry Advocacy & Insight, The Value Exchange, and Co-lead of the Settlement Technical Workstream and SSI Taskforce, EU T+1 Industry Committee. Firms therefore need to identify SSI exceptions they have today and work to resolve them to combat the build-up of operational, settlement and regulatory risk.

Johnson cautioned against the EU pursuing a centralised SSI database. Building a central utility in the available time is not realistic, she argued. And while it might ease the standardisation problem within the region, it could entrench differences and complexity rather than promote a global standard.

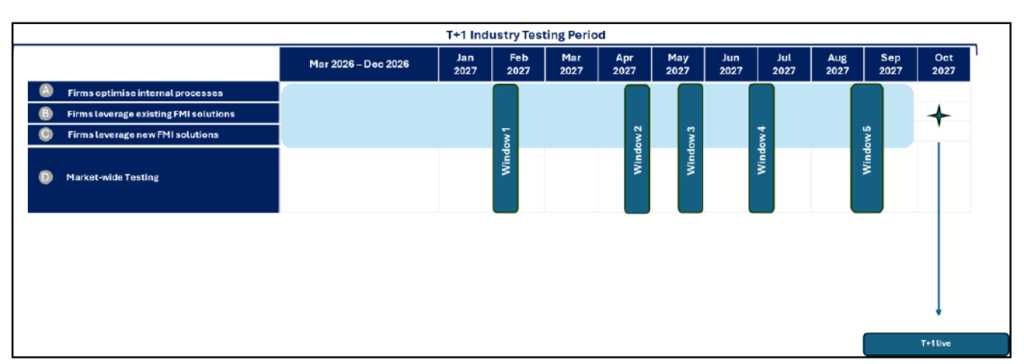

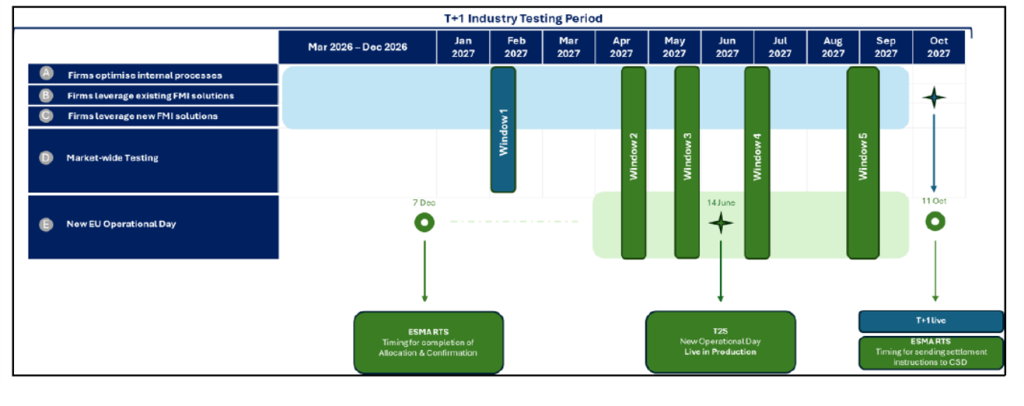

Navigating the transition to T+1 in Europe: What is the plan for industry testing?

As we count down to the October 2027 T+1 transition, testing the industry’s readiness will increasingly come to the fore. To underpin that process, the EU, UK and Swiss T+1 taskforces recently published a joint document setting out a coordinated testing strategy.

As panel moderator James Maher observed, the strategy deliberately avoids prescribing an exhaustive set of testing requirements for every firm, and instead balances guidance with giving firms flexibility to design testing appropriate to their operating models.

The testing plan revolves around five pillars, according to speakers at the event:

- Internal testing – of any of the changes firms make internally to prepare for T+1.

- Adoption of existing FMI settlement efficiency tools – leveraging available capabilities such as partial settlement.

- Adoption of new FMI functionality – for instance, the introduction of same-day stock lending issuance and reports.

- Market-wide testing – five testing windows of two to three weeks each are scheduled for February to September 2027, during which the Taskforce encourages all FMIs and, where relevant, the settlement agents and intermediaries to offer their test environments.

- New EU operational day (including the EU gating event) – which will see some FMIs changing their timings e.g. for their nighttime settlement batch. Testing for the new operational day can only happen from April 2027, once T2S and some of the European infrastructures are ready.

Maher added that while the T2S enhancements won’t be completed by the February 2027 window, it can be used to test corporate actions, as the other four windows are in the middle of corporate action season. “There will be a lot of strain on corporate action teams in 2027, so I would strongly encourage firms to use the February window,” he said. Firms also need to take steps to “derisk the transition.” The Taskforce came up with four high-level metrics to help:

- Assess your rate of allocations/confirmations completed by the UK/EU deadlines.

- Check instruction input timing to ensure you can meet the recommendations of no later than midnight in Europe and 06:00 in the UK.

- Examine your matching rate.

- Evaluate your settlement efficiency under T+2 today to see what you need to improve so you can do on T+0 what you currently achieve by T+1.

Alongside internal assessments, firms can check these metrics against available industry rates, the audience heard, which stands as a good gap analysis to see what steps need to be taken when navigating the transition to T+1 in Europe.

FAQs

When does T+1 in Europe go live?

The UK, EU and Swiss markets will switch to T+1 settlement on 11 October 2027, as discussed at the ‘Towards T+1 in Europe – from Regulation to Reality’ event.

What interim deadlines are there before the October 2027 go live?

The EU and UK have both recommended that by 31 December 2026 all trade allocations and confirmations between buy side firms and executing brokers be completed no later than 23:00 CET on the trade date in Europe and 23:59 GMT in the UK. The EU is expected to include this as a requirement in an amended RTS on Settlement Discipline, due later this year, whilst in the UK, the FCA has indicated it could demand evidence that firms’ plans and any outsourcing arrangements are compliant.

How does T+1 settlement in Europe affect FX?

T+1 pulls the FX process forward, so managers need the base currency available earlier and may use pre funding or tighter intraday liquidity procedures to gain funding certainty.

How does T+1 settlement in Europe affect fund settlement cycles?

For EU exposed funds, the recommendation is to shift to a T+2 fund settlement cycle, while APAC focused funds should contend with a thin overlap window (15:00 CET equals 22:00 JST), which reduces liquidity and widens bid ask spreads for end investors.

What operational changes do asset managers need for T+1 in Europe?

All post trade activities move to the trade date, requiring a review of end to end workflows, verification of the Place of Safekeeping (PSAF) and early agreement on the Place of Settlement (PSET), and the adoption of partial settlement. Existing FX models must be evaluated for suitability, with many firms likely delegating FX to custodians or third party providers, and allocations and confirmations should be sent within a three-to-four-hour window after execution to move toward near real time processing. Full automation and the removal of end of day batch allocations are now “table stakes,” while Standard Settlement Instructions (SSIs) must be cleaned up because 21% to 30% of securities fails are SSI related.

What is the testing strategy for T+1 in Europe?

The industry testing programme is built on five pillars:

• Internal testing of each firm’s changes.

• Adoption of existing FMI settlement efficiency tools such as partial settlement.

• Adoption of new FMI functionality like same day stock lending issuance.

• Market wide testing across five windows of two to three weeks each scheduled from February to September 2027.

• Testing the new EU operational day (including the gating event) from April 2027 once T2S upgrades are live.

Firms are also asked to monitor four high level metrics: allocation/confirmation rates, instruction input timing (midnight CET/06:00 GMT), matching rate, and current T+2 settlement efficiency—to “derisk” the transition.