What

are social bonds? How do they differ from conventional bonds and green bonds?

And why have issuers and investors turned to them during the pandemic?

To

answer the last question first, Covid-19 is drastically altering the economic

and financial landscape. Rising fatality rates are focusing attention on the

funding of overstretched healthcare systems, while enforced lockdowns mean

companies are facing liquidity constraints and questions about their long-term

viability. As policymakers worldwide set out comprehensive packages in response

to this crisis, social bonds are a key tool to help finance those measures.

Like

green bonds, social bonds are a type of sustainable bond, with the capital

raised used to fund defined projects, which must be reported. (Capital raised

in conventional bonds may be used for general purposes and there is no

reporting.) Unlike green bonds, these defined projects have a primarily social,

rather than an environmental, objective. Unlike green bonds, issuance volumes

have until now been low.

Their

popularity has changed with the onset of the pandemic: social bonds have seen a

spike in supply, with supranational institutions and national development

agencies driving issuance volumes (see box, “The Covid-19 response bonds”).

|

How has the social bond market developed in the past year? In July 2019, investors were found to be gradually building their social bond portfolios, but lack of supply was hindering the creation of dedicated social bond funds. Despite growing interest, the social bond market has remained small, hindered by a lack of liquidity and a perceived lack of clarity in reporting standards. Social bond issuance reached $14.0 billion in 2019, accounting for only 5% of the sustainable bond market. This compared to $217 billion of green bond issuances, topping 80% of the market. The pandemic-induced shift in demand for social bonds in 2020 shows issuance volumes reaching $33.1 billion at the end of April this year, compared with $6.2 billion in the same period last year. Looking at market share in 2020, green bonds currently account for 50% of the sustainable bond market compared to 28% for social bonds, indicating a rebalancing effect between the two closely related products.  Source: Bloomberg, BNP Paribas, as of 24th April 2020 |

What most of these recent issues have in common is a use-of-proceeds framework that follows the International Capital Markets Association’s (ICMA) Social Bond Principles (SBP) [1].Depending on the terms of each bond, money raised from investors will be directed to anything from alleviating the financial pressure on healthcare systems to providing targeted financial support and liquidity to companies. The SBPs outline issuers’ obligations, including project evaluation and selection, management of proceeds and reporting. This has the benefit of giving investors focused on environmental, social and governance objectives the confidence that their ESG needs are met.

Before Covid-19, social bonds were being used to fund various projects ranging from infrastructure and social services to housing and employment generation. Since the onset of the pandemic, they have been identified as relevant for financing efforts to tackle the recovery – including the financing of new medical equipment, repurposing factories to produce essential equipment and providing financial support to businesses so they can retain staff and employment levels.

|

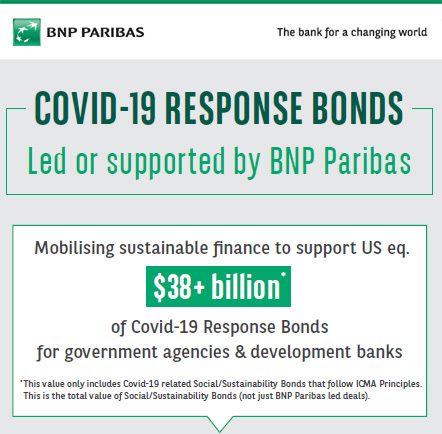

The Covid-19 response bonds The flurry of social and social-themed bonds issued by supranational and agency development institutions in response to Covid-19 is a trend expected to continue in the coming months as other issuers – financial institutions and corporates – monitor this market. We may also see a second wave of social bonds focused more on the medium-term response.

|

Rebalance: social or green?

There is a significant rebalancing of the sustainable bond market towards social debt, according to Agnès Gourc, Co-Head of Sustainable Finance Markets at BNP Paribas. “The crisis has caused a huge shake-up in financial markets and has acted as a big stimulus for social bonds,” she explains. “A change in investor behaviour could also see the demand continue for years to come as investors look to incorporate more ESG into their portfolios, shifting the focus to the social element in light of recent events.”

While the social bond market is likely to continue its growth path, investor interest in green bonds will nonetheless remain high: the climate crisis will continue to be a pressing issue.

|

Banks, the economy and purpose “In response to the health crisis, the Group’s teams have mobilised around the world to contribute to the functioning of the economy and its financing. Our concerns have been to protect our employees who are fully mobilised to ensure banking services, to quickly implement solutions to support the financing of our corporate, institutional and individual clients, and to launch in all regions where we are present a plan for emergency donations to the hospital sector and organisations committed to assist vulnerable people.” Jean-Laurent Bonnafé, Chief Executive Officer, BNP Paribas Group |

How this rebalancing between social bonds and green bonds exactly plays out remains to be seen. Climate change should be expected to remain high on the political agenda, with continuing investor support for green bonds.

In Europe, all eyes will be on the implementation of the EU Taxonomy regulation, according to Gourc. Conversely, the current rise in social bonds could have a lasting impact on both investors’ and issuers’ approaches to the market, she explains. This could lead to pressure for a “just transition”, given how starkly the current crisis has exposed inequalities, while using this new opportunity to reset the world economies in a greener way.

[1] BNP Paribas is a member of the ICMA GBP SBP Executive Committee, and a member of the ICMA Social Bond Principles Working Group